Have you ever stopped to analyze how financial advice and budgeting tips can change the way you handle your money in your daily life?

Today you will see the main financial advice and budgeting tips that are truly applicable to the reality of attractive interest rates and new tax limits is essential for those who wish not only to survive, but to prosper.

Our goal is financial advice and budgeting tips that will help you better control your money on a daily basis. Keep reading.

Financial advice and budgeting tips

1. Pillars that make a difference in your financial life (Financial advice and budgeting tips)

Building sustainable financial health is never the result of a single stroke of luck. Good financial health is only built with disciplined good habits in financial control.

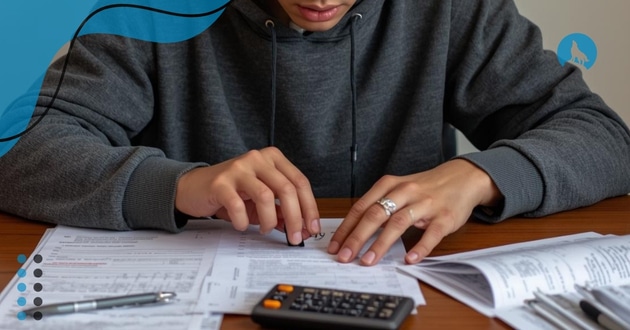

The first step for any solid plan is to coldly analyze your net income. A frequent mistake in managing your money is confusing gross salary with real liquidity.

Your budget should invariably start by calculating the amount effectively deposited after all mandatory deductions, such as federal and state taxes, and social security.

For freelancers and gig economy workers, the complexity is greater and requires a “lowest common denominator” approach, where the budget is based on the lowest billing month of the last 12 to 24 months, not the arithmetic average.

2. The 50/30/20 Method will change your financial life

The 50/30/20 method remains an efficient standard for those seeking balance, allocating:

- 50% of income for necessities such as housing and food;

- 30% for discretionary wants;

- 20% strictly for savings and debts.

However, in high-cost metropolitan areas, keeping necessities below half of income has become a challenge that requires adjustments to housing expectations.

Having problems with financial control? Then you need to know the financial tips for families.

3. The right way to protect your assets

In an unstable economic scenario, asset protection has ceased to be a luxury and has become a necessity.

The first step is to build a solid emergency fund, capable of sustaining three to six months of essential expenses, such as housing, fixed bills, and insurance.

Here’s a tip! For families with a single income or professionals exposed to market instability. The ideal approach is to expand this reserve to six to nine months of essential expenses. Ensuring greater financial security and stability.

It’s not enough just to save: where the money is kept makes all the difference.

Currently, high-yield savings accounts (HYSAs) stand out as the most efficient option, with annual returns between 4% and 5%.

They preserve purchasing power against inflation. Maintain immediate liquidity for daily financial needs. They reduce the risk of misuse by remaining separated from the checking account, strengthening financial control and security.

At the same time, you must attack the greatest enemy of wealth, high-cost debts. Credit cards with interest rates above 20% erode any attempt at investment. Eliminate these debts before investing.

Finally, the annual review of insurance is essential.

Inflation has raised the costs of real estate and vehicles, making many policies outdated. For those with greater wealth, umbrella insurance expands protection against civil liabilities, while disability insurance is crucial.

4. Retirement Optimization and Succession Planning (Financial advice and budgeting tips)

With debts under control and the emergency reserve structured, the next step is to optimize retirement.

The absolute priority should be to take advantage of the employer match in 401(k) plans. This benefit is equivalent to an immediate return of up to 100% on the invested amount — ignoring it is giving up guaranteed money.

Currently, there are many brokers, such as Fidelity, that offer good returns.

You should bear in mind that diversification between Traditional and Roth accounts is a key strategy. After all, it creates tax flexibility in the future, allowing you to combine taxable income and tax-exempt income in retirement, according to the economic scenario and the tax bracket at the time.

Succession planning has ceased to be exclusive to large fortunes and has become part of basic financial responsibility.

For this reason, an efficient plan starts with three essential documents: Will, Durable Power of Attorney, and Advance Health Care Directive.

Together, they guarantee the correct distribution of assets, avoid family conflicts, and prevent judicial intervention in sensitive medical decisions.

Planning for retirement and succession is not just about thinking about the future, but about organizing today for fiscal efficiency, family security, and the continuity of wealth.

Main Options for Affordable Retirement Housing

1. Sun City Hilton Head – South Carolina (Financial advice and budgeting tips)

Sun City Hilton Head is one of the largest and most complete 55+ communities in the United States, located in the charming Lowcountry of South Carolina.

It functions as a planned and self-sufficient city, ideal for those seeking quality of life, leisure, and social integration in retirement.

The great differential is the scale of the amenities. The heart of the community is a 45-acre Village Center, integrated with a Central Plaza with a clock tower, which concentrates events, meetings, and daily activities.

Social life is intense and well-structured, with more than 100 clubs and associations, ranging from arts and ceramics to civic debates and politics, allowing each resident to find their space and build real connections.

2. On Top of the World – Florida

Located in Ocala, this is one of Florida’s largest and oldest private communities.

Because it is inland, it offers natural protection against coastal storms. The highlight of On Top of the World is its unique amenities. They include a private field for model airplane flying, a drone course, and the “Master the Possibilities” education center.

The community is interconnected by golf cart paths, allowing access to services without the use of automobiles.

Financially, it presents itself as a more accessible option than coastal ones, with competitive condo fees that cover robust exterior maintenance, including roof repair in some neighborhoods.

3. Valle Verde – California (Financial advice and budgeting tips)

Representing the CCRC and Life Plan Community segment, Valle Verde is situated in the Mediterranean climate of Santa Barbara.

Currently, the 63-acre campus prioritizes ground-floor garden homes instead of vertical density.

Its advantage is the continuum of care: independent living, assisted living, memory support, and skilled nursing in the same location. This ensures that residents never need to move due to declining health.

The financial model requires a significant entrance fee. Functioning as long-term care insurance, it offers intimacy and privacy rare in CCRCs.

Conclusion

Throughout this guide, it became clear that applying financial advice and budgeting tips strategically is the safest way to achieve stability, protect assets, and plan the future with confidence.

It all starts with real control of net income, goes through effective methods like the 50/30/20, and is strengthened by creating a well-structured emergency fund.

Furthermore, the elimination of high-cost debts, the correct choice of high-yield accounts, and the periodic review of insurance form the basis of asset protection.

With this structure, it is possible to move forward to retirement optimization, taking advantage of benefits such as employer match and tax diversification.

Finally, the conscious choice of affordable housing options in retirement completes an integrated, practical, and sustainable financial vision for the long term.